In short: Indian pharma AI adoption is mid-way through the curve, which means three things at once: some commercial teams are already in production, some are stuck in proof-of-concept, and some have not started. The gap between them is rarely the model. It is org design, data readiness, and the engineering work of getting a pilot to production.

There is a number that has been circulating in Indian pharma boardrooms for about eighteen months now. It says, in various forms, that roughly half of Indian pharmaceutical companies are still at proof-of-concept stage with AI. The number is approximate, the methodology is informal, and the boundary between proof-of-concept and production is contested. But the directional reading holds: by the end of 2025, in the country that supplies twenty percent of the global generics market, AI adoption is somewhere near the middle of the curve. Not at the start. Not at the finish. Mid-way.

The phrase "mid-way through" is doing some real work in that sentence. It means three different things at once, and the boardrooms that are most useful to be in are the ones that hold all three at the same time.

It means a meaningful number of Indian pharma commercial teams are running AI in production today. Not in slide decks. Not in pilots that have been alive for eighteen months. In production. Models re-ranking a Territory Manager's call plan each cycle from recent Rx trend and competitor signal. Foundation-model-assisted reconciliation of primary, secondary, IQVIA, and SMSRC to a single territory master. Retrieval over the company's own sales reports and brand plans, queryable in plain language by a Brand Manager. These are not edge cases; they are the most boring AI workflows in the world; they are also among the most expensive ones we could possibly automate, and they ship.

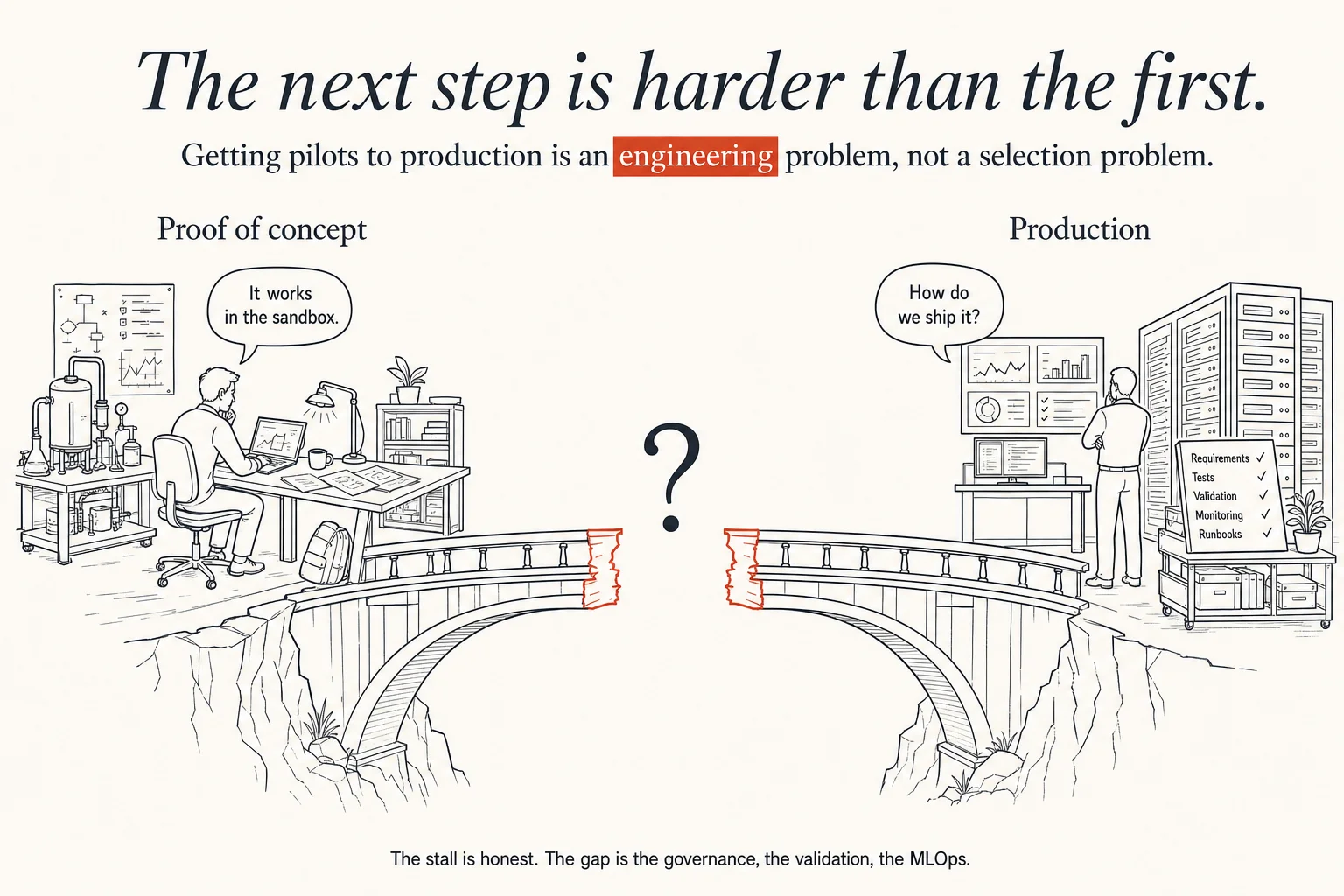

It also means a much larger number of commercial teams have started a pilot, run it for six to nine months, learned what they would do differently, and stalled before going to production. The stall is rarely about the model. It is about the data, the governance, the validation, the MLOps, the procurement process, the tolerance the team has for an AI recommendation that sends an MR to the wrong doctor or misreads a quarter's secondary sales. The stall is mid-way honestly because the next step is harder than the first one, not easier.

And it means a third set of commercial teams, in the same companies, have not started. Next-best-action recommendations the MR actually trusts in the field. Analysis of RCPA and chemist feedback at scale, across languages. Real-time detection of competitor share shifts from the IQVIA and SMSRC streams. These are workloads where AI would matter, and where the engineering and data work to get there has not begun.

Why the framing matters

The reason "mid-way through" is useful, rather than just descriptive, is that it predicts what the next twelve months will be about. A market at the start of adoption is dominated by demonstrations: can the model do this at all. A market at the end of adoption is dominated by competition: who deploys this better than whom. A market in the middle is dominated by something quieter and more uncomfortable, which is the work of getting the second half of pilots to production.

That work is engineering work, not vendor-selection work. It is the work of MLOps discipline, evaluation infrastructure, data governance, human-in-the-loop design, and the patient negotiation between a commercial head and her IT counterpart over what counts as "ready to ship." It does not have a single named buyer. The buyer is the Chief Commercial Officer and the Head of Sales Excellence and the Chief Information Officer and the GM of Data and Infrastructure, sitting in a room together, deciding whether a system that has worked for nine months in a sandbox can be allowed to touch a single byte of live customer and prescription data.

That room is the room AI for Pharma is being convened to host.

The stall is mid-way honestly because the next step is harder than the first one, not easier.

— The view from the room we are trying to host.

Three forces that make 2026 different

If 2024 and 2025 were the years of "can AI do this?" inside Indian pharma, 2026 looks different on three fronts. None of these is a prediction in the marketing sense. Each is an observation about what has already shifted, that the second half of the curve is being held back by, and that the next twelve months are likely to test.

One: foundation models are now good enough for the commercial decision

The single largest unlock of the past two years, for Indian pharma commercial teams specifically, is that the current generation of frontier language models, GPT, Claude, Gemini, are good enough at reading messy commercial data and explaining a recommendation that the gap between "model output" and "the version a Brand Manager would act on" is now a review problem, not a generation problem. This is a quiet but enormous change. A year ago, the bottleneck was the model. Today, the bottleneck is the human review loop, the eval, the data reconciliation, the audit trail back to source.

The implication is concrete: the procurement conversation that mattered in 2024 (which model, which vendor, what does it cost per token) matters considerably less in 2026 than the engineering conversation (what is our eval set, how do we route uncertain cases, how do we trace every number back to a primary, secondary, IQVIA, or SMSRC source). Indian pharma commercial teams that have figured this out are already moving from proof-of-concept to production. Teams still negotiating model contracts are running the wrong meeting.

Two: the governance question moves from "can we?" to "how do we?"

In 2024, the dominant governance question inside Indian pharma commercial teams was binary. Can we put customer and prescriber data through a hosted foundation model? Can we let an AI system recommend which doctors an MR visits? Can we trust a model's territory attribution enough to set a target on it? The answers were cautious, inherited, and almost always conservative.

In 2026, the question is no longer binary. The data-residency and customer-data questions have answers now, the named US vendors clear procurement, and commercial leaders have watched a peer ship something that worked. The governance question is not "can we?" but "how do we?" How do we document the eval set for a call-plan model? How do we treat a recommendation the MR can override versus one the system acts on? How do we trace every number in a Brand Manager's review back to a primary, secondary, IQVIA, or SMSRC source? These are answerable questions, and the companies that answer them best will be deploying AI in places their peers are still asking permission to enter.

This is exactly the shift that the consortium is intended to host. The "can we?" conversation could happen between a commercial team and its own IT department. The "how do we?" conversation requires the commercial head, the AI engineer who built the system, the data and infrastructure team, and the field leader whose numbers it will move, all in the same room.

Three: the procurement question moves from IT to function

There is one structural change in Indian pharma's AI adoption that is undersold and important. AI procurement has, until recently, been an IT decision. The IT organisation evaluated platforms, negotiated contracts, selected tools, and rolled them out to functions. This worked when AI was infrastructure. It does not work, anymore, when AI is workflow.

What has changed is that AI workloads with the highest production value are workflow-shaped, not infrastructure-shaped. They live inside a specific commercial function (sales, marketing, sales excellence, commercial analytics), they use that function's domain language, they require that function's domain experts to evaluate and improve them, and they are deployed against that function's KPIs: Rx share, coverage, secondary movement, market share against IQVIA. The IT organisation is necessary but not sufficient. The Head of Sales Excellence or the Brand Manager is making the decisions that used to be made by the Head of IT.

This is part of the reason the AI for Pharma application asks the applicant which commercial function they lead, and what AI question is on their desk right now. The function is the unit of decision, and the room we are building reflects that.

What it means for the next twelve months

Putting the three forces together, here is what we expect the next twelve months to look like inside the kinds of Indian pharma companies we are building the room for.

First, the gap between leading and lagging companies will widen, faster, in 2026 than it did in 2024 or 2025. Leading companies have already crossed the production-engineering threshold for one or two workloads; the next workloads are easier because the platform and the eval discipline already exist. Lagging companies, the ones still negotiating their first procurement contract, are starting from zero on a curve that is now steeper.

Second, the most useful conversations will not happen at large industry conferences. They will happen between specific function leaders at specific companies who are running specific workloads against specific datasets. The pattern that closes the gap is peer-to-peer, narrow, and recurring. Conferences broadcast; consortia convene; the difference matters more in a market mid-way through adoption than in a market at the start.

Third, the questions that get asked will get more concrete. A year ago the question was "how can we use AI?" Today it is "how do we get our call-plan model to handle the territories it currently routes to manual review, and reconcile SMSRC with IQVIA before it does?" That question has a real answer; the answer is engineering work and eval work; the engineering work and eval work has been done somewhere else by someone the asker has not yet met. Closing that gap, deliberately, is the unit of value the consortium is designed to produce.

Why we are convening this

AI for Pharma is being convened in 2026 because the structure of the conversation has changed and the existing rooms have not changed with it. Pharma trade associations were built for a different cadence and a different mandate. Tech conferences host a much larger and much less specific audience. Vendor user-group meetings host the function but never the peer competitor who has already shipped it. None of those rooms is wrong; none of them is the room a Head of Sales Excellence needs to be in when she is trying to put a call-plan optimisation system into the field next quarter.

We are convening because that specific room does not yet exist in India, because we have been having most of these conversations bilaterally for a year, and because the consortium model, three to four editions a year, single-day, single-room, by application, is the right size and the right cadence for the conversation that 2026 will turn out to need.

The first edition is forthcoming. The application is open. The room is small on purpose.